In the ever-evolving world of finance, the persistent menace of banking fraud looms large, posing a formidable challenge to both financial institutions and their customers. The year 2021 bore witness to a startling surge in online banking fraud cases across India, with over 4,800 incidents reported. This marked a significant increase from the previous year, highlighting a troubling trend. As banking operations have increasingly migrated to digital platforms, so too have the methods of fraudsters, who have honed their skills in using sophisticated digital techniques to breach customer identities and gain unauthorised access to personal accounts. To maintain the trust of their existing clientele and draw in new customers, banks must harness cutting-edge technology to strengthen their defences against financial fraud in this digital age.

Tales of Common Banking Fraud

*The Deceptive Art of Phishing*: Picture this—a seemingly innocuous email lands in your inbox, or perhaps it’s a text message on your phone or a voice on the other end of a call, all claiming to be from your bank. These fraudsters, skilled in the art of deception, craft messages designed to lure you into clicking on a malicious link, inadvertently downloading malware onto your device, or divulging sensitive personal information. Phishing, a cunning form of social engineering, often lays the groundwork for more elaborate banking fraud schemes.

*Identity Theft: The Shadowy Impersonation*: Imagine waking up one day to find that your identity has been stolen. This insidious form of fraud involves wrongfully acquiring someone’s personal information and exploiting it for unlawful purposes. Stolen identities are frequently employed in account takeover attacks, where criminals seize control of a victim’s online account, leaving the actual account holder locked out and bewildered.

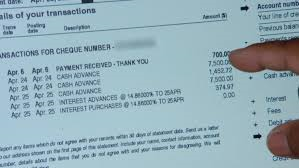

*The Silent Plunder of Credential Theft*: Credential theft has high stakes. It begins with the stealthy acquisition of a customer’s banking information—details that extend beyond mere personal facts to include confidential data like ID numbers, passwords, and Social Security numbers. With these stolen credentials in hand, fraudsters are poised to execute account takeovers, leaving unsuspecting victims in their wake.

*The Intricacies of Wire Fraud*: Imagine the intricate dance of telecommunications as perpetrators weave their web of deceit through wire fraud. They manipulate communication channels to orchestrate fraudulent transactions, leaving victims entangled in a complex web of financial loss.

In this unfolding narrative of banking fraud, financial institutions are called upon to remain vigilant and innovative, employing advanced technologies and strategies to combat these ever-present threats. Only by doing so can they hope to protect their customers and secure their place in the trust-driven world of finance.

Once upon a time, in the intricate world of finance, there existed a cunning breed of villains known as wire fraudsters. These tricksters wove their deceitful webs through telecommunication lines and the vast expanse of the internet, preying on unsuspecting individuals. Disguised as desperate family members or friends in urgent need, they lured banking customers into transferring their hard-earned money to faraway lands.

Meanwhile, in the shadowy underbelly of the financial realm, another group of rogues engaged in money laundering. These crafty criminals devised elaborate schemes to cloak the origins, proceeds, and nature of their unlawful activities through a series of complex financial transactions. Their actions not only threatened the very fabric of the banking industry but also ensnared innocent institutions in their nefarious networks.

Not far behind were the devious masterminds of application fraud. With stolen or fabricated identities in hand, these swindlers boldly applied for loans or lines of credit. Once granted access, they cunningly maintained a façade of normalcy, using their accounts just like any other customer. But when the moment was right, they vanished into thin air, leaving behind substantial debts and empty coffers.

As time marched on, new forms of trickery emerged from the shadows, such as the ominous “Fraud as a Service” and the elusive art of biometrics spoofing. These developments underscored the ever-present need for vigilance within the banking sector, urging guardians of finance to remain alert and proactive.

In response to these threats, a noble quest for bank fraud detection and prevention was undertaken. Financial institutions gathered their wisest minds to forge a robust shield against deceit. This shield was composed of a tapestry of policies, protocols, procedures, and cutting-edge technologies—all designed to protect their treasures and loyal patrons from fraudulent foes.

The detection armoury was meticulously crafted, equipped to monitor lurking dangers and scrutinise accounts with a discerning eye. It sought to unravel behavioural patterns and identify risks before they could wreak havoc. On the prevention side, proactive measures were employed—internal controls were fortified, employees trained as vigilant sentinels and multi-layered security measures erected as formidable barriers.

In this relentless battle against fraud, banks understood that they must outwit their adversaries by weaving advanced technology into their defences. The legendary power of Artificial Intelligence (AI) was called upon to enhance their strategies. Unlike traditional methods that relied on rigid rules, AI brought adaptability to the table, evolving alongside emerging threats and offering a dynamic shield against the forces of deception.

In this tale of intrigue and strategy, banks continue their quest to safeguard their domain from the ever-looming spectre of fraud, determined to stay one step ahead in the eternal dance between light and shadow.

Once upon a time, in the ever-evolving world of finance, banks faced a relentless adversary: fraud. Traditional fraud monitoring systems were like ancient guardians, relying on rigid rules etched in stone. These systems, though once practical, could not keep pace with the cunning tactics of modern-day fraudsters. Their inflexible nature meant they could only sound the alarm after the deed was done, often mistaking innocent actions for foul play and leaving customers frustrated.

But then, a new hero emerged on the horizon—Artificial Intelligence. This technological marvel arrived like a wise sage, capable of sifting through mountains of data with the speed of light. Unlike its predecessors, AI could detect fraudulent activities as they unfolded, adapting swiftly to the ever-changing landscape of threats. Banks found solace in AI’s ability to fine-tune their defences, significantly reducing false alarms and enhancing customer satisfaction.

In the realm of AI, there lived a powerful ally known as Machine Learning. This apprentice of AI was endowed with the gift of learning from experience. By analysing patterns from behavioural data and gathering insights from various sources, machine learning empowered banks to anticipate and thwart fraud before it struck, safeguarding both customers and treasures.

As the story unfolded, another noble technique joined the battle—Biometric Authentication. This method relied on the distinct physical traits of individuals, such as voices, faces, or fingerprints, to confirm identities. Although not invincible to all trickery, when paired with other security measures, biometrics offered a formidable shield against fraudsters’ schemes.

In this tale of security, Two-Factor and Multi-Factor Authentication played key roles as well. These methods required individuals to present multiple proofs of identity, creating layers of protection that were difficult to penetrate. When combined with other technologies, these authentication processes formed an impenetrable fortress against fraudulent activities.

And so, in this epic saga of innovation and defence, Advanced Analytics became the storyteller’s secret weapon. With each transaction that passed through the financial kingdom’s gates, vast amounts of data were generated. By employing sophisticated techniques to analyse this treasure trove of information, banks gained a comprehensive understanding of their operations and fortresses.

Together, these technological champions ensured that banks could navigate the treacherous waters of fraud with confidence and grace. In doing so, they not only protected their realms but also fostered trust and peace among their patrons, allowing them to thrive in a world where security reigned supreme.

In the bustling world of finance, where transactions flow ceaselessly like a mighty river, banks find themselves awash with data. This vast ocean of information holds secrets waiting to be uncovered. By harnessing the power of advanced data science, financial institutions can dive deep beneath the surface, revealing a comprehensive view of their operations. This exploration not only streamlines their processes but also equips them with the foresight to anticipate and thwart fraudulent schemes, fortifying their defences against the ever-present threat of deception.

In this relentless battle against fraud, banks face formidable challenges. The masterminds of fraud are cunning and ever-evolving, constantly finding new ways to bypass existing security barriers. To counter this, banks must remain vigilant, perpetually updating their security protocols. They conduct regular training sessions for their staff to keep them informed about the latest threats and closely watch emerging patterns in banking fraud.

With the advent of digital banking channels, a new frontier has opened up—one that is both promising and perilous. Online and mobile banking platforms have become fertile ground for cybercriminals who employ sophisticated tactics such as malware, phishing, and hacking to pilfer sensitive information and masquerade as unsuspecting customers.

Yet, banks must tread carefully in their quest for security. The delicate balance between safeguarding their systems and ensuring a seamless customer experience is crucial. While stringent authentication measures can deter fraudsters, they also risk alienating genuine customers, potentially leading to dissatisfaction and loss of clientele.

Amidst this intricate dance of security and service, financial institutions navigate the labyrinthine world of compliance. The banking sector is tightly regulated, demanding strict adherence to a web of guidelines designed to detect and prevent fraud. This involves regular audits, continuous staff training, and sometimes even overhauling business practices. Failure to comply can result in severe consequences, including hefty fines, damage to reputation, and erosion of customer trust.

One particularly insidious form of fraud is money laundering, a shadowy process through which illicit funds are made to appear legitimate. Banks deploy robust systems to identify suspicious activities, scrutinise customer behaviour, and analyse transaction patterns, all while conducting thorough due diligence on their clientele.

Thus unfolds the story of modern banking—a tale of vigilance and innovation, where technology and tradition intertwine to protect the sanctity of financial transactions in an ever-changing landscape.

The Tale of the Banking Battleground

Once upon a time, in the intricate world of finance, there existed a shadowy practice known as money laundering. This clandestine art involved transforming ill-gotten gains into seemingly legitimate funds, posing a formidable challenge to the guardians of financial institutions. These custodians, the banks, had devised elaborate systems to thwart such deceptions. They meticulously scrutinised customer behaviour and transaction patterns, employing rigorous due diligence to unearth any suspicious activities. Yet, as the cunning strategies of money launderers evolved, so did the banks’ need to continually enhance their defences.

In another corner of this financial realm, the journey of welcoming new customers was a pivotal moment. The process of onboarding was not just a gateway to services but also a first impression that could make or break a potential relationship. A labyrinthine or tedious entry could dissuade prospective patrons. Thus, banks faced the delicate task of crafting an onboarding experience that balanced security with simplicity. They needed to verify the integrity of new clients without burdening them with excessive complexities.

Meanwhile, lurking in the shadows was the menace of credential theft—a sinister plot in which nefarious actors sought to pilfer customer login details. To combat this threat, banks embarked on an educational campaign, enlightening their clientele about the perils of sharing passwords and the importance of safe online practices. They fortified their digital fortresses with safeguards like automatic logouts and account locks after multiple failed attempts. However, even the most fortified bastions could not entirely shield customers from external dangers like phishing scams.

In this dynamic landscape, the sentinels of banking fraud detection laid out their battle plans. They fortified their strongholds with robust internal controls, employing dual controls, regular audits, and meticulous vetting procedures to detect and thwart fraudulent schemes. Empowering their customers was also paramount; banks shared knowledge about fraud tactics and security measures, offering tools for vigilant account monitoring and alerts for unusual activities.

The vigilant eyes of transaction monitoring systems scanned for anomalies—be it huge sums, rapid sequences of transactions, or sudden shifts in device or location. These systems raised alarms at the slightest hint of deceit. Moreover, banks harnessed the power of real-time data enrichment tools, drawing insights from myriad sources to identify suspicious patterns swiftly.

As the final bastion against fraud’s relentless advance, banks deployed the cutting-edge forces of machine learning and artificial intelligence. These technological marvels tirelessly analysed data to uncover complex fraud schemes that might have otherwise slipped through unnoticed.

And so, in this ever-evolving saga of banking security, the defenders continued their vigilant watch, adapting and innovating to protect their realm from those who sought to exploit its vulnerabilities.

Secure browsing

When it comes to staying safe online, using a secure and private browser is crucial. Such a browser can help protect your personal information and keep you safe from cyber threats. One option that offers these features is the Maxthon Browser, which is available for free. It comes with built-in Adblock and anti-tracking software to enhance your browsing privacy.

By utilising Maxthon Browser, users can browse the internet confidently, knowing that their online activities are shielded from prying eyes. The integrated security features alleviate concerns about potential privacy breaches and ensure a safer browsing environment. Furthermore, the browser’s user-friendly interface makes it easy for individuals to customise their privacy settings according to their preferences.

Maxthon Browser not only delivers a seamless browsing experience but also prioritises the privacy and security of its users through its efficient ad-blocking and anti-tracking capabilities. With these protective measures in place, users can enjoy the internet while feeling reassured about their online privacy.

In addition, the desktop version of Maxthon Browser works seamlessly with their VPN, providing an extra layer of security. By using this browser, you can minimise the risk of encountering online threats and enjoy a safer internet experience. With its combination of security features, Maxthon Browser aims to provide users with peace of mind while they browse.

Maxthon Browser is a reliable choice for users who prioritise privacy and security. With its robust encryption measures and extensive privacy settings, it offers a secure browsing experience that gives users peace of mind. The browser’s commitment to protecting user data and preventing unauthorised access sets it apart in the competitive web browser market.